Usage-based insurance analyzes driving behaviors such as speed, acceleration, and braking patterns to tailor premiums, promoting safer driving habits. Mileage-based insurance calculates premiums primarily on the number of miles driven, offering cost savings for low-mileage drivers. Discover how these innovative insurance models can optimize your coverage and savings.

Why it is important

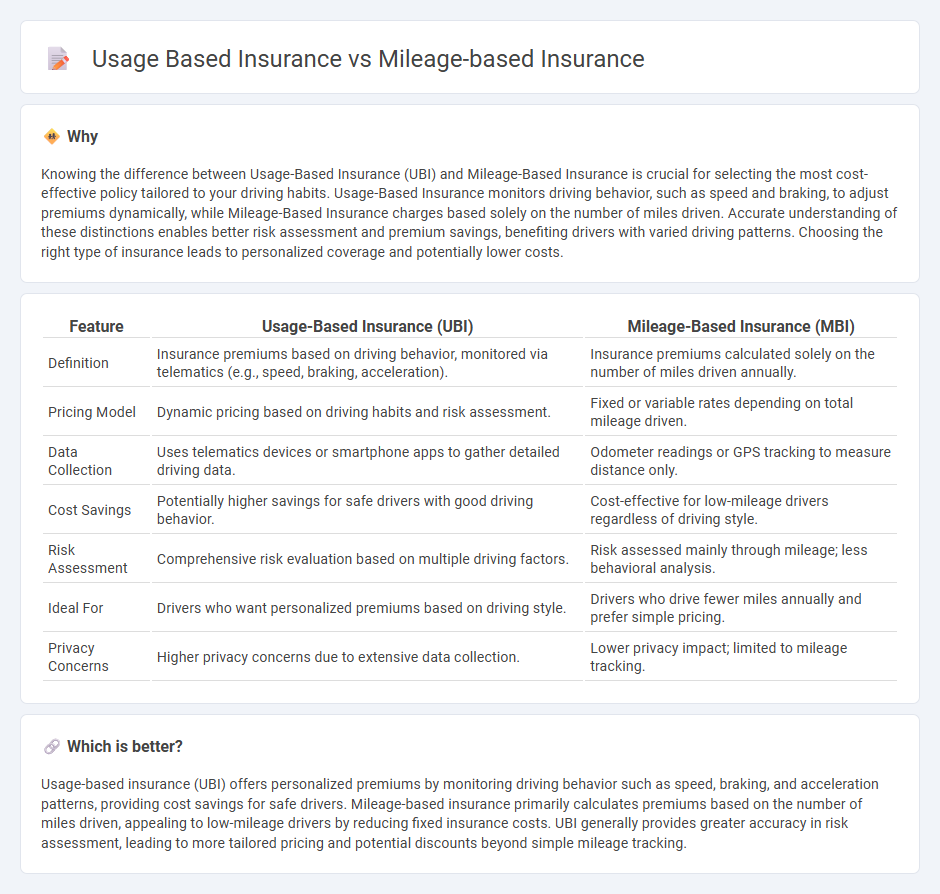

Knowing the difference between Usage-Based Insurance (UBI) and Mileage-Based Insurance is crucial for selecting the most cost-effective policy tailored to your driving habits. Usage-Based Insurance monitors driving behavior, such as speed and braking, to adjust premiums dynamically, while Mileage-Based Insurance charges based solely on the number of miles driven. Accurate understanding of these distinctions enables better risk assessment and premium savings, benefiting drivers with varied driving patterns. Choosing the right type of insurance leads to personalized coverage and potentially lower costs.

Comparison Table

| Feature | Usage-Based Insurance (UBI) | Mileage-Based Insurance (MBI) |

|---|---|---|

| Definition | Insurance premiums based on driving behavior, monitored via telematics (e.g., speed, braking, acceleration). | Insurance premiums calculated solely on the number of miles driven annually. |

| Pricing Model | Dynamic pricing based on driving habits and risk assessment. | Fixed or variable rates depending on total mileage driven. |

| Data Collection | Uses telematics devices or smartphone apps to gather detailed driving data. | Odometer readings or GPS tracking to measure distance only. |

| Cost Savings | Potentially higher savings for safe drivers with good driving behavior. | Cost-effective for low-mileage drivers regardless of driving style. |

| Risk Assessment | Comprehensive risk evaluation based on multiple driving factors. | Risk assessed mainly through mileage; less behavioral analysis. |

| Ideal For | Drivers who want personalized premiums based on driving style. | Drivers who drive fewer miles annually and prefer simple pricing. |

| Privacy Concerns | Higher privacy concerns due to extensive data collection. | Lower privacy impact; limited to mileage tracking. |

Which is better?

Usage-based insurance (UBI) offers personalized premiums by monitoring driving behavior such as speed, braking, and acceleration patterns, providing cost savings for safe drivers. Mileage-based insurance primarily calculates premiums based on the number of miles driven, appealing to low-mileage drivers by reducing fixed insurance costs. UBI generally provides greater accuracy in risk assessment, leading to more tailored pricing and potential discounts beyond simple mileage tracking.

Connection

Usage-based insurance (UBI) and mileage-based insurance both utilize telematics technology to monitor driving behavior and distance traveled, enabling insurers to tailor premiums according to actual usage patterns. Mileage-based insurance specifically calculates rates primarily on the number of miles driven, while UBI incorporates broader data such as driving style, time, and location to assess risk more comprehensively. Both models aim to promote safer driving habits and offer cost savings by aligning insurance costs with individual driving behavior.

Key Terms

Telematics

Mileage-based insurance calculates premiums primarily on the total miles driven annually, offering savings for low-mileage drivers by assessing risk through distance alone. Usage-based insurance (UBI) leverages telematics technology to monitor detailed driving behaviors such as speed, acceleration, braking, and time of day, providing a more personalized and accurate risk profile. Explore how telematics-driven UBI transforms insurance pricing models and enhances driving safety.

Premium calculation

Mileage-based insurance calculates premiums strictly on the total miles driven, using odometer readings or GPS data to assess driving distance. Usage-based insurance incorporates a wider range of driving behaviors like speed, braking patterns, and time of day alongside mileage, creating a more personalized risk profile. Explore more about how these premium calculations affect your insurance costs and potential savings.

Driving behavior

Mileage-based insurance calculates premiums primarily on the total miles driven annually, offering straightforward savings for low-mileage drivers. Usage-based insurance (UBI) incorporates real-time driving behavior data such as speed, acceleration, braking patterns, and time of day to more accurately assess risk and personalize rates. Explore how telematics and advanced analytics enhance policy precision and customer benefits.

Source and External Links

Pay-Per-Mile Car Insurance: What You Should Know - Pay-per-mile insurance charges a base rate plus a per-mile fee, offering flexibility for low-mileage drivers.

Pay-Per-Mile Car Insurance with SmartMiles - SmartMiles by Nationwide offers pay-per-mile insurance with rates based on mileage, providing savings for low-mileage drivers.

Best Pay-Per-Mile Car Insurance Options (2025) - Provides an overview of pay-per-mile insurance options, highlighting their suitability for low-mileage drivers.