Reciprocal insurance involves a group of subscribers who exchange insurance contracts to share risks, typically managed by an attorney-in-fact, providing personalized underwriting and flexible policies. Fraternal benefit societies are nonprofit organizations offering insurance and social benefits exclusively to members who share a common affiliation, such as religion or ethnicity, emphasizing community and mutual aid. Discover how these unique insurance models can offer tailored coverage and benefits suited to different needs.

Why it is important

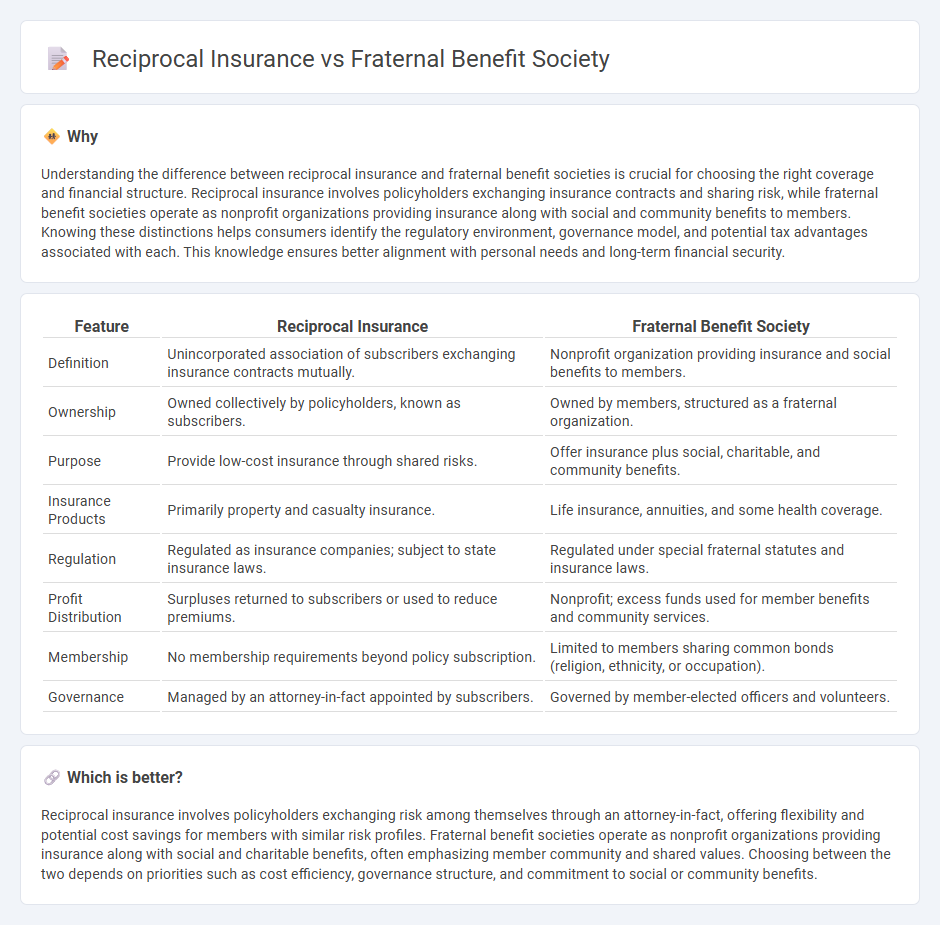

Understanding the difference between reciprocal insurance and fraternal benefit societies is crucial for choosing the right coverage and financial structure. Reciprocal insurance involves policyholders exchanging insurance contracts and sharing risk, while fraternal benefit societies operate as nonprofit organizations providing insurance along with social and community benefits to members. Knowing these distinctions helps consumers identify the regulatory environment, governance model, and potential tax advantages associated with each. This knowledge ensures better alignment with personal needs and long-term financial security.

Comparison Table

| Feature | Reciprocal Insurance | Fraternal Benefit Society |

|---|---|---|

| Definition | Unincorporated association of subscribers exchanging insurance contracts mutually. | Nonprofit organization providing insurance and social benefits to members. |

| Ownership | Owned collectively by policyholders, known as subscribers. | Owned by members, structured as a fraternal organization. |

| Purpose | Provide low-cost insurance through shared risks. | Offer insurance plus social, charitable, and community benefits. |

| Insurance Products | Primarily property and casualty insurance. | Life insurance, annuities, and some health coverage. |

| Regulation | Regulated as insurance companies; subject to state insurance laws. | Regulated under special fraternal statutes and insurance laws. |

| Profit Distribution | Surpluses returned to subscribers or used to reduce premiums. | Nonprofit; excess funds used for member benefits and community services. |

| Membership | No membership requirements beyond policy subscription. | Limited to members sharing common bonds (religion, ethnicity, or occupation). |

| Governance | Managed by an attorney-in-fact appointed by subscribers. | Governed by member-elected officers and volunteers. |

Which is better?

Reciprocal insurance involves policyholders exchanging risk among themselves through an attorney-in-fact, offering flexibility and potential cost savings for members with similar risk profiles. Fraternal benefit societies operate as nonprofit organizations providing insurance along with social and charitable benefits, often emphasizing member community and shared values. Choosing between the two depends on priorities such as cost efficiency, governance structure, and commitment to social or community benefits.

Connection

Reciprocal insurance exchanges operate as unincorporated groups where members insure each other, sharing risk and premiums collectively. Fraternal benefit societies function similarly by providing insurance benefits to their members, often tied to a common affiliation such as a religious or ethnic group. Both structures emphasize member-driven risk pooling and mutual financial support, distinguishing them from traditional stock insurance companies.

Key Terms

Membership (Fraternal Society)

Fraternal benefit societies operate as nonprofit organizations primarily serving their members, who share common bonds such as religion, ethnicity, or profession, and emphasize member participation in governance and benefits. Their membership model fosters a strong sense of community and mutual support, distinguishing them from reciprocal insurance exchanges, which function through inter-policyholder agreements without a formal membership structure. Explore further to understand how these unique membership frameworks impact benefits and policyholder relations.

Attorney-in-Fact (Reciprocal)

Fraternal benefit societies are member-owned organizations offering insurance and social benefits, whereas reciprocal insurance operates through an Attorney-in-Fact, a managing entity that administers policies on behalf of its subscribers. The Attorney-in-Fact in reciprocal insurance handles underwriting, claims, and administrative tasks, leveraging contractual authority granted by members, which distinguishes it from the member-management model of fraternal societies. Explore the detailed roles and regulatory frameworks governing Attorneys-in-Fact to understand the operational mechanics of reciprocal insurance.

Certificate of Insurance

Fraternal benefit societies issue a Certificate of Insurance as proof of membership benefits, often highlighting nonprofit status and community focus, while reciprocal insurance exchanges provide certificates emphasizing their unique risk-sharing agreements among insured parties. Certificates in fraternal societies typically detail member rights and privileges, whereas reciprocal insurance certificates emphasize policy terms and mutual liability coverage. Explore how these distinct certificates impact policyholder protections and service expectations for deeper insight.

Source and External Links

Benefit society - Wikipedia - A fraternal benefit society is a not-for-profit membership organization with a lodge system, offering life insurance and other benefits to members united by common bonds such as religion, ethnicity, or occupation; such societies are exempt from income tax under Section 501(c)(8) of the U.S. Tax Code and engage in social, charitable, and educational activities.

fraternal benefit society benefits | Wex - Law.Cornell.Edu - These societies provide members with mutual financial assistance including life or health insurance and sometimes community aid; they have historically played a key role in social welfare before government programs and remain tax-exempt under 501(c)(8).

What is a Fraternal Insurance Company? Learn with BetterLife - Fraternal benefit societies are not-for-profit groups organized by local chapters that provide life and disability insurance to members sharing common bonds, operate democratically, and reinvest surplus funds in member benefits and charitable community work.