Alternative credit data expands the scope of borrower evaluation by incorporating non-traditional financial behaviors such as utility payments, rental history, and digital transaction records, enhancing credit scoring accuracy beyond conventional metrics. Peer-to-peer lending data provides granular insights from direct loan transactions between individuals, reflecting real-time repayment behavior and social trust factors within lending communities. Explore how these innovative data sources redefine risk assessment and credit access in modern banking.

Why it is important

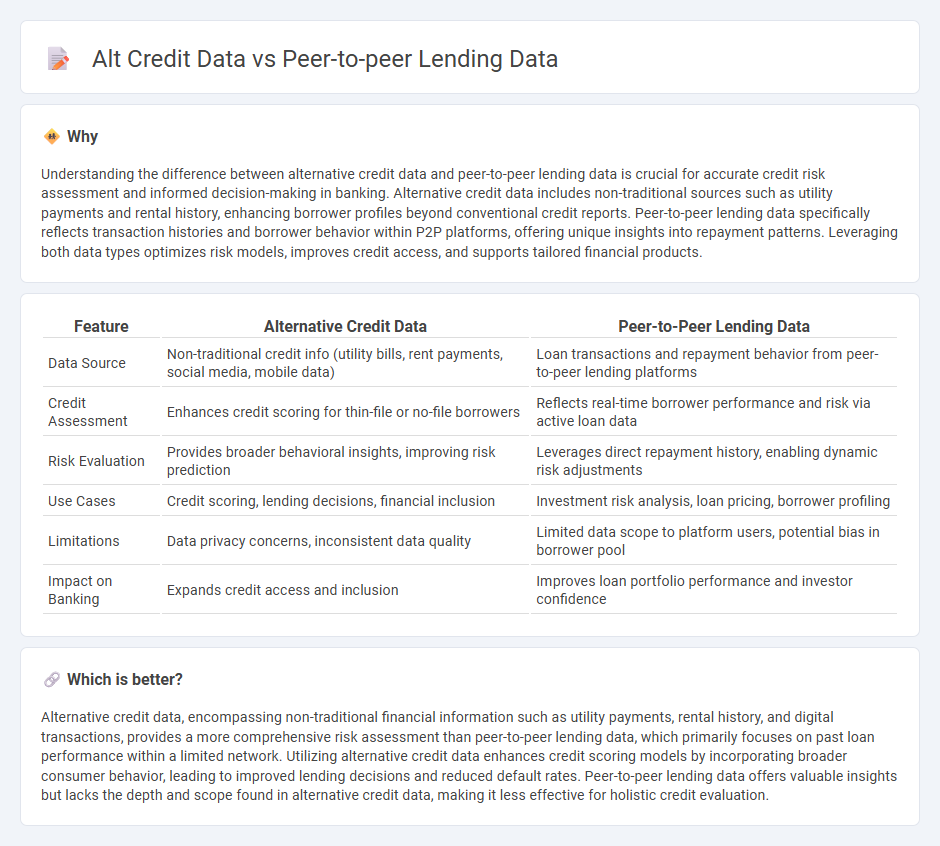

Understanding the difference between alternative credit data and peer-to-peer lending data is crucial for accurate credit risk assessment and informed decision-making in banking. Alternative credit data includes non-traditional sources such as utility payments and rental history, enhancing borrower profiles beyond conventional credit reports. Peer-to-peer lending data specifically reflects transaction histories and borrower behavior within P2P platforms, offering unique insights into repayment patterns. Leveraging both data types optimizes risk models, improves credit access, and supports tailored financial products.

Comparison Table

| Feature | Alternative Credit Data | Peer-to-Peer Lending Data |

|---|---|---|

| Data Source | Non-traditional credit info (utility bills, rent payments, social media, mobile data) | Loan transactions and repayment behavior from peer-to-peer lending platforms |

| Credit Assessment | Enhances credit scoring for thin-file or no-file borrowers | Reflects real-time borrower performance and risk via active loan data |

| Risk Evaluation | Provides broader behavioral insights, improving risk prediction | Leverages direct repayment history, enabling dynamic risk adjustments |

| Use Cases | Credit scoring, lending decisions, financial inclusion | Investment risk analysis, loan pricing, borrower profiling |

| Limitations | Data privacy concerns, inconsistent data quality | Limited data scope to platform users, potential bias in borrower pool |

| Impact on Banking | Expands credit access and inclusion | Improves loan portfolio performance and investor confidence |

Which is better?

Alternative credit data, encompassing non-traditional financial information such as utility payments, rental history, and digital transactions, provides a more comprehensive risk assessment than peer-to-peer lending data, which primarily focuses on past loan performance within a limited network. Utilizing alternative credit data enhances credit scoring models by incorporating broader consumer behavior, leading to improved lending decisions and reduced default rates. Peer-to-peer lending data offers valuable insights but lacks the depth and scope found in alternative credit data, making it less effective for holistic credit evaluation.

Connection

Alt credit data and peer-to-peer lending data intersect by providing alternative sources of borrower information beyond traditional credit reports, enhancing risk assessment in banking. Peer-to-peer lending platforms generate unique financial behavior data such as repayment patterns and social signals, which feed into alt credit data models to predict creditworthiness more accurately. This integration enables banks to expand credit access to underbanked populations while minimizing default risks through enriched data analytics.

Key Terms

Creditworthiness Assessment

Peer-to-peer lending data primarily includes borrower profiles, repayment history, and platform-specific behavioral metrics essential for evaluating creditworthiness, whereas alternative credit data leverages unconventional sources such as utility payments, rental history, and social media activity to complement traditional assessments. Both data types aim to reduce default risk by providing a comprehensive view of a borrower's financial behavior and reliability. Explore how integrating these data sources can enhance creditworthiness assessments and improve lending decisions.

Borrower Risk Profiling

Peer-to-peer lending data offers insights directly from borrower transaction histories and repayment behaviors, enabling granular risk profiling focused on individual creditworthiness. Alternative credit data, including utility payments, rental histories, and social data, broadens risk assessment by incorporating non-traditional indicators often unavailable in P2P platforms, enhancing prediction models for underbanked populations. Discover how leveraging both data types can refine borrower risk profiles and improve lending decisions.

Alternative Data Sources

Alternative data sources in peer-to-peer lending include social media activity, utility payment history, and mobile phone usage patterns, offering richer insights beyond traditional credit reports. These datasets enhance risk assessment models, enabling lenders to identify creditworthy borrowers who lack conventional credit history. Explore how integrating alternative credit data transforms lending accuracy and financial inclusion.

Source and External Links

Dataset from the US Peer-to-peer Lending Platform with Macroeconomic Variables - Mendeley Data - This dataset aggregates United States state-level data from LendingClub's loan book from 2008-2019, providing over two million observations with loan, borrower, and state-specific features for cross-sectional and longitudinal analyses.

Peer-to-peer lending to small businesses - Federal Reserve Board - The paper analyzes LendingClub loan-level data, focusing on small business loan applications, funding rates, loan sizes, interest rates, and delinquency, compared to traditional lending sources.

Peer to Peer (P2P) Lending Market Size and Forecast 2025 to 2034 - Precedence Research - Reports the global P2P lending market size (USD 176.5 billion in 2025), growth projections (up to USD 1,380.8 billion by 2034), and notes the industry's reliance on AI and machine learning for risk assessment and borrower-lender matching.