Environmental Social Governance (ESG) accounting integrates environmental, social, and governance factors into financial analysis, highlighting corporate sustainability and ethical impact. Social accounting focuses specifically on measuring social performance and stakeholder engagement, emphasizing transparency and social responsibility. Explore how these accounting approaches differ and contribute to comprehensive corporate reporting.

Why it is important

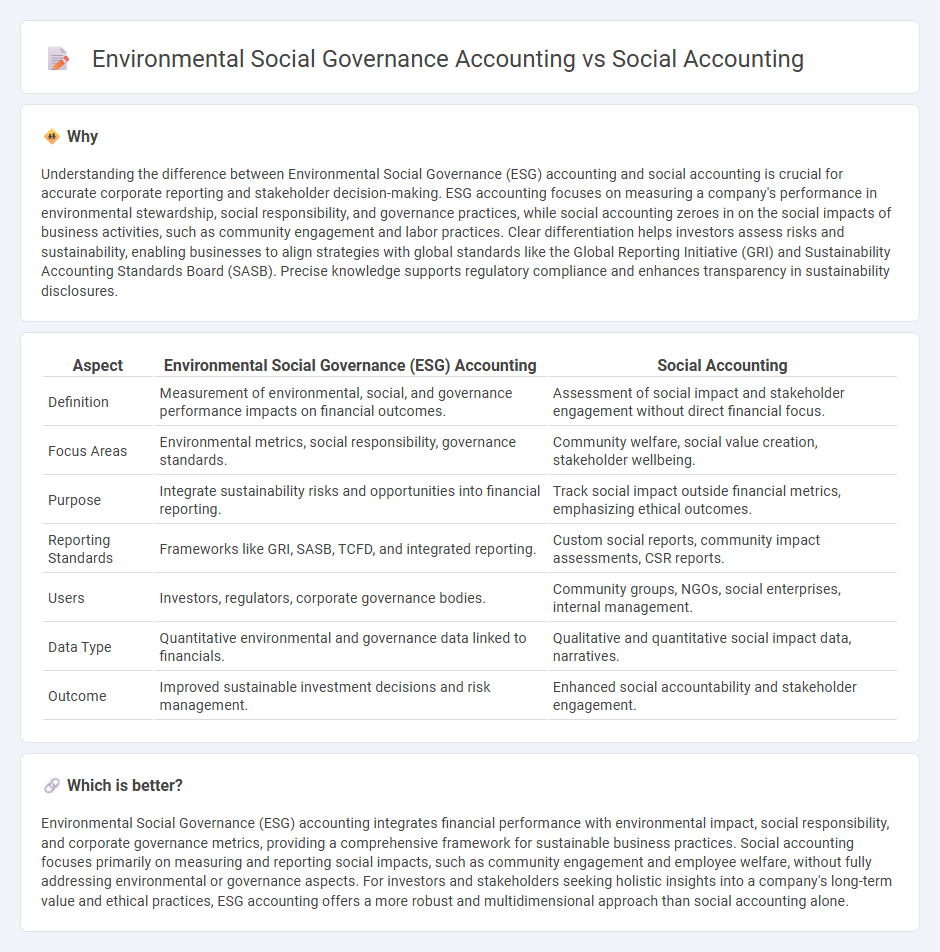

Understanding the difference between Environmental Social Governance (ESG) accounting and social accounting is crucial for accurate corporate reporting and stakeholder decision-making. ESG accounting focuses on measuring a company's performance in environmental stewardship, social responsibility, and governance practices, while social accounting zeroes in on the social impacts of business activities, such as community engagement and labor practices. Clear differentiation helps investors assess risks and sustainability, enabling businesses to align strategies with global standards like the Global Reporting Initiative (GRI) and Sustainability Accounting Standards Board (SASB). Precise knowledge supports regulatory compliance and enhances transparency in sustainability disclosures.

Comparison Table

| Aspect | Environmental Social Governance (ESG) Accounting | Social Accounting |

|---|---|---|

| Definition | Measurement of environmental, social, and governance performance impacts on financial outcomes. | Assessment of social impact and stakeholder engagement without direct financial focus. |

| Focus Areas | Environmental metrics, social responsibility, governance standards. | Community welfare, social value creation, stakeholder wellbeing. |

| Purpose | Integrate sustainability risks and opportunities into financial reporting. | Track social impact outside financial metrics, emphasizing ethical outcomes. |

| Reporting Standards | Frameworks like GRI, SASB, TCFD, and integrated reporting. | Custom social reports, community impact assessments, CSR reports. |

| Users | Investors, regulators, corporate governance bodies. | Community groups, NGOs, social enterprises, internal management. |

| Data Type | Quantitative environmental and governance data linked to financials. | Qualitative and quantitative social impact data, narratives. |

| Outcome | Improved sustainable investment decisions and risk management. | Enhanced social accountability and stakeholder engagement. |

Which is better?

Environmental Social Governance (ESG) accounting integrates financial performance with environmental impact, social responsibility, and corporate governance metrics, providing a comprehensive framework for sustainable business practices. Social accounting focuses primarily on measuring and reporting social impacts, such as community engagement and employee welfare, without fully addressing environmental or governance aspects. For investors and stakeholders seeking holistic insights into a company's long-term value and ethical practices, ESG accounting offers a more robust and multidimensional approach than social accounting alone.

Connection

Environmental Social Governance (ESG) accounting and Social Accounting are interconnected through their shared focus on non-financial performance measurement, emphasizing a company's social and environmental responsibilities. Both frameworks incorporate metrics that assess social impact, sustainability practices, and stakeholder engagement, providing comprehensive insights beyond traditional financial statements. Integrating ESG accounting with Social Accounting enhances transparency, accountability, and supports sustainable business practices aligned with corporate social responsibility (CSR) goals.

Key Terms

**Social Accounting:**

Social accounting measures a company's impact on society by tracking metrics such as employee well-being, community engagement, and social equity initiatives. It emphasizes transparency in social value creation and stakeholder relationships, distinct from Environmental Social Governance (ESG) accounting which integrates environmental and governance factors alongside social metrics. Explore in-depth insights into how social accounting drives sustainable business practices and stakeholder trust.

Stakeholder Reporting

Social accounting emphasizes measuring an organization's social impact and responsibilities toward stakeholders, including community engagement, labor practices, and human rights. Environmental Social Governance (ESG) accounting integrates environmental sustainability metrics, social responsibility, and corporate governance into financial reporting, providing a comprehensive view of a company's impact on stakeholders and long-term value creation. Explore how stakeholder reporting evolves by incorporating ESG frameworks to enhance transparency and accountability.

Social Impact Assessment

Social accounting measures an organization's social impact through metrics such as community engagement, employee well-being, and stakeholder relationships. Environmental Social Governance (ESG) accounting expands this focus by integrating environmental performance, social responsibility, and corporate governance into comprehensive sustainability reporting. Explore further to understand how these frameworks shape responsible business strategies and impact societal outcomes.

Source and External Links

The Difference between Social Accounting and Social Auditing - Social accounting is a systematic process for measuring, reporting, and verifying an organization's social and environmental impacts, emphasizing transparency and accountability to stakeholders.

Social accounting - Wikipedia - Social accounting communicates the social and environmental effects of organizations' economic actions to interest groups and society at large, focusing on corporate accountability beyond traditional financial metrics.

Social Accounting: A Practical Guide - Community-Wealth.org - Social accounting involves three main steps: planning (identifying key elements), accounting (designing and conducting the system), and reporting and responding (sharing results with stakeholders and acting on findings).