Real-time expense recognition records expenses as they are incurred, providing an accurate financial picture aligned with business activities, while cash basis accounting records transactions only when cash changes hands, potentially delaying expense recognition. This method improves financial transparency and aids in timely decision-making, contrasting with the simplicity and immediate cash flow focus of cash basis accounting. Explore the differences in accounting accuracy and financial management between these approaches to enhance your business strategies.

Why it is important

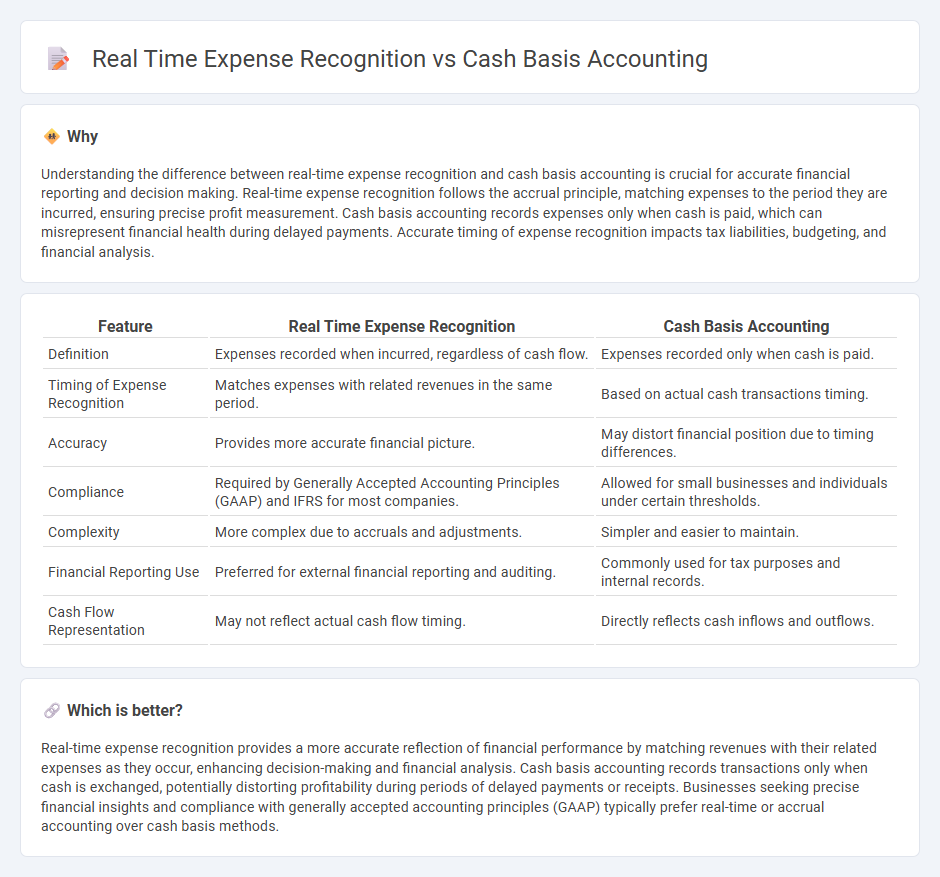

Understanding the difference between real-time expense recognition and cash basis accounting is crucial for accurate financial reporting and decision making. Real-time expense recognition follows the accrual principle, matching expenses to the period they are incurred, ensuring precise profit measurement. Cash basis accounting records expenses only when cash is paid, which can misrepresent financial health during delayed payments. Accurate timing of expense recognition impacts tax liabilities, budgeting, and financial analysis.

Comparison Table

| Feature | Real Time Expense Recognition | Cash Basis Accounting |

|---|---|---|

| Definition | Expenses recorded when incurred, regardless of cash flow. | Expenses recorded only when cash is paid. |

| Timing of Expense Recognition | Matches expenses with related revenues in the same period. | Based on actual cash transactions timing. |

| Accuracy | Provides more accurate financial picture. | May distort financial position due to timing differences. |

| Compliance | Required by Generally Accepted Accounting Principles (GAAP) and IFRS for most companies. | Allowed for small businesses and individuals under certain thresholds. |

| Complexity | More complex due to accruals and adjustments. | Simpler and easier to maintain. |

| Financial Reporting Use | Preferred for external financial reporting and auditing. | Commonly used for tax purposes and internal records. |

| Cash Flow Representation | May not reflect actual cash flow timing. | Directly reflects cash inflows and outflows. |

Which is better?

Real-time expense recognition provides a more accurate reflection of financial performance by matching revenues with their related expenses as they occur, enhancing decision-making and financial analysis. Cash basis accounting records transactions only when cash is exchanged, potentially distorting profitability during periods of delayed payments or receipts. Businesses seeking precise financial insights and compliance with generally accepted accounting principles (GAAP) typically prefer real-time or accrual accounting over cash basis methods.

Connection

Real-time expense recognition enhances cash basis accounting by recording transactions precisely when cash is exchanged, improving financial accuracy and cash flow management. This approach minimizes timing discrepancies between expense occurrence and payment, ensuring up-to-date financial statements. Accurate tracking supports better budgeting and decision-making by reflecting actual cash movements promptly.

Key Terms

Timing of Recognition

Cash basis accounting records expenses only when cash is paid, leading to delayed recognition of costs. Real-time expense recognition captures expenses immediately as they are incurred, providing a more accurate financial picture. Explore the impact of timing on financial decision-making and compliance by learning more about these accounting methods.

Accrual vs. Cash

Cash basis accounting records expenses and revenues only when cash is exchanged, providing a straightforward view of cash flow but potentially delaying expense recognition. Real-time expense recognition, aligned with accrual accounting principles, records expenses as they are incurred regardless of payment timing, offering a more accurate financial picture for decision-making. Explore the detailed differences between accrual and cash basis methods to optimize your accounting strategy.

Matching Principle

Cash basis accounting records expenses only when cash is paid, which can distort financial results by failing to match expenses with the revenues they generate within the same period. Real-time expense recognition aligns with the Matching Principle by recording expenses when incurred, ensuring financial statements accurately reflect the economic activity of a business. Explore comprehensive insights on how these accounting methods impact financial transparency and decision-making.

Source and External Links

Cash Basis Accounting: Definition, Example, Pros and Cons - Cash basis accounting is a method that records income only when cash is received and expenses only when cash is paid, mostly used by small, cash-based businesses and not accepted under GAAP or IFRS.

What Is Cash Basis Accounting? Definition and Guide - This method tracks revenue and expenses only when cash changes hands, making it suitable for very small businesses or individuals dealing mostly in cash.

Cash-based accounting: A guide to the cash basis - Cash-based accounting recognizes revenues and expenses only when money is actually received or paid, focusing on cash flow rather than accounts receivable or payable.