Algorithmic compliance in accounting ensures standardized adherence to regulatory frameworks through automated data analysis, minimizing human error and enhancing efficiency. Auditor judgment involves expert interpretation and critical evaluation of financial statements to identify risks and anomalies that algorithms might overlook. Discover how balancing algorithmic compliance with auditor judgment can optimize financial accuracy and regulatory adherence.

Why it is important

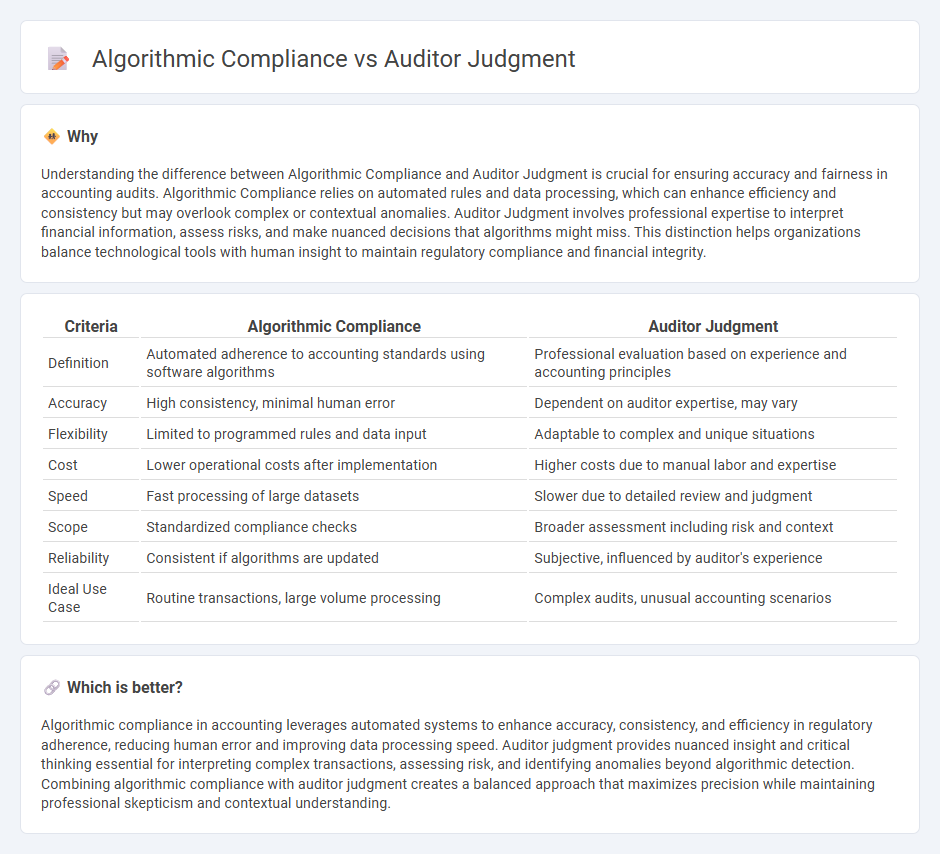

Understanding the difference between Algorithmic Compliance and Auditor Judgment is crucial for ensuring accuracy and fairness in accounting audits. Algorithmic Compliance relies on automated rules and data processing, which can enhance efficiency and consistency but may overlook complex or contextual anomalies. Auditor Judgment involves professional expertise to interpret financial information, assess risks, and make nuanced decisions that algorithms might miss. This distinction helps organizations balance technological tools with human insight to maintain regulatory compliance and financial integrity.

Comparison Table

| Criteria | Algorithmic Compliance | Auditor Judgment |

|---|---|---|

| Definition | Automated adherence to accounting standards using software algorithms | Professional evaluation based on experience and accounting principles |

| Accuracy | High consistency, minimal human error | Dependent on auditor expertise, may vary |

| Flexibility | Limited to programmed rules and data input | Adaptable to complex and unique situations |

| Cost | Lower operational costs after implementation | Higher costs due to manual labor and expertise |

| Speed | Fast processing of large datasets | Slower due to detailed review and judgment |

| Scope | Standardized compliance checks | Broader assessment including risk and context |

| Reliability | Consistent if algorithms are updated | Subjective, influenced by auditor's experience |

| Ideal Use Case | Routine transactions, large volume processing | Complex audits, unusual accounting scenarios |

Which is better?

Algorithmic compliance in accounting leverages automated systems to enhance accuracy, consistency, and efficiency in regulatory adherence, reducing human error and improving data processing speed. Auditor judgment provides nuanced insight and critical thinking essential for interpreting complex transactions, assessing risk, and identifying anomalies beyond algorithmic detection. Combining algorithmic compliance with auditor judgment creates a balanced approach that maximizes precision while maintaining professional skepticism and contextual understanding.

Connection

Algorithmic compliance enhances the accuracy and consistency of financial reporting by automating rule-based audit procedures, which supports auditors in focusing their professional judgment on complex or subjective areas. Auditor judgment remains crucial in interpreting algorithm outputs, assessing risks, and applying ethical considerations to ensure regulatory compliance and financial integrity. This synergy between algorithmic tools and auditor expertise strengthens audit quality and reduces the risk of errors or fraud.

Key Terms

Professional Skepticism

Professional skepticism remains a critical element in auditor judgment, enabling nuanced evaluation beyond algorithmic compliance checks. While algorithms efficiently handle rule-based compliance, they cannot replicate the auditor's ability to interpret complex financial contexts and identify subtle anomalies. Explore how integrating professional skepticism with advanced technology enhances audit quality and reliability.

Decision Rules

Auditor judgment involves subjective evaluation based on professional experience and contextual nuances, while algorithmic compliance relies on predefined decision rules and data-driven models to ensure consistency and scalability. Decision rules in algorithmic compliance reduce human bias and enhance regulatory adherence by applying standardized criteria across cases. Explore more about optimizing regulatory processes through the balance of human expertise and algorithmic decision rules.

Consistency

Auditor judgment offers nuanced decision-making that adapts to complex scenarios, while algorithmic compliance ensures consistency by strictly following predefined rules and eliminating human bias. Algorithms provide scalable solutions with standardized outputs, reducing variability across audits but may lack context sensitivity found in experienced auditors. Explore further to understand how combining both approaches can enhance compliance and reliability in auditing processes.

Source and External Links

The Importance of Auditor Judgment in Improving Audit Quality - This paper explores how auditor judgment affects audit quality, emphasizing its necessity in the audit process.

Professional Judgment Resource - This resource highlights the significance of professional judgment in audit quality by enhancing independence, objectivity, and professional skepticism.

The Auditor's Professional Judgment Process - This framework outlines the steps and factors influencing auditors' professional judgment, emphasizing its central role in the audit process.