Instant payments provide real-time fund transfers 24/7 with immediate confirmation, contrasting with NEFT (National Electronic Funds Transfer), which operates in hourly batches during bank business hours. While NEFT is widely accepted for inter-bank transfers with structured settlement timings, instant payments enhance speed and convenience for urgent transactions. Explore the detailed comparison between instant payments and NEFT to choose the best option for your banking needs.

Why it is important

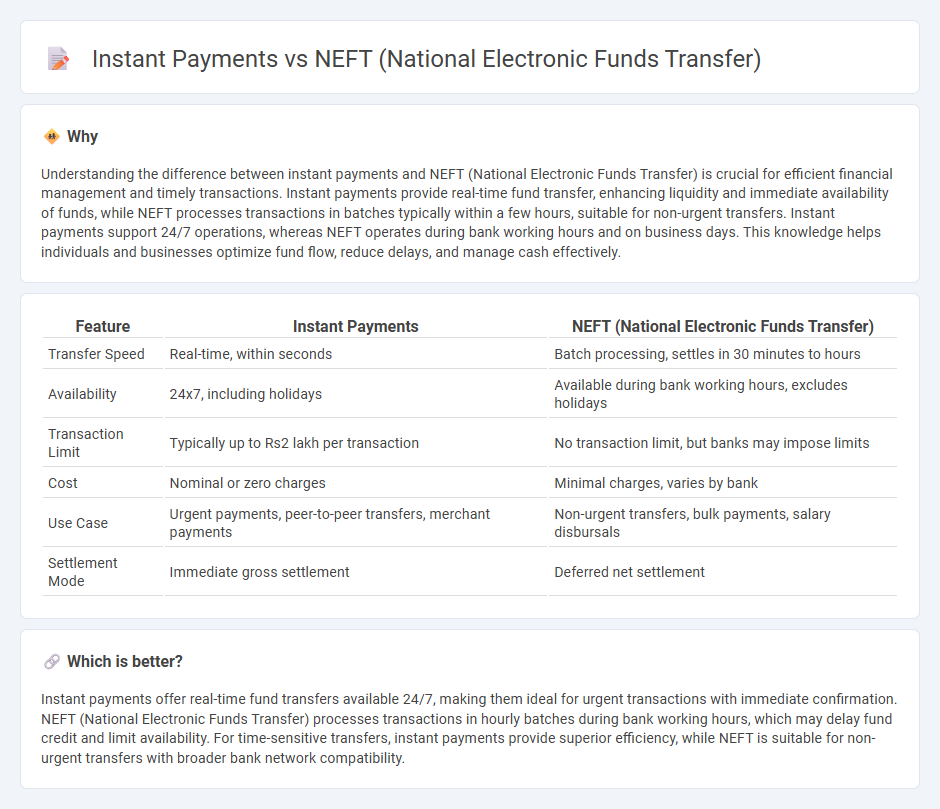

Understanding the difference between instant payments and NEFT (National Electronic Funds Transfer) is crucial for efficient financial management and timely transactions. Instant payments provide real-time fund transfer, enhancing liquidity and immediate availability of funds, while NEFT processes transactions in batches typically within a few hours, suitable for non-urgent transfers. Instant payments support 24/7 operations, whereas NEFT operates during bank working hours and on business days. This knowledge helps individuals and businesses optimize fund flow, reduce delays, and manage cash effectively.

Comparison Table

| Feature | Instant Payments | NEFT (National Electronic Funds Transfer) |

|---|---|---|

| Transfer Speed | Real-time, within seconds | Batch processing, settles in 30 minutes to hours |

| Availability | 24x7, including holidays | Available during bank working hours, excludes holidays |

| Transaction Limit | Typically up to Rs2 lakh per transaction | No transaction limit, but banks may impose limits |

| Cost | Nominal or zero charges | Minimal charges, varies by bank |

| Use Case | Urgent payments, peer-to-peer transfers, merchant payments | Non-urgent transfers, bulk payments, salary disbursals |

| Settlement Mode | Immediate gross settlement | Deferred net settlement |

Which is better?

Instant payments offer real-time fund transfers available 24/7, making them ideal for urgent transactions with immediate confirmation. NEFT (National Electronic Funds Transfer) processes transactions in hourly batches during bank working hours, which may delay fund credit and limit availability. For time-sensitive transfers, instant payments provide superior efficiency, while NEFT is suitable for non-urgent transfers with broader bank network compatibility.

Connection

Instant payments and NEFT (National Electronic Funds Transfer) are crucial components of modern banking that facilitate electronic funds transfer between bank accounts. While NEFT processes transactions in hourly batches during designated hours, instant payments enable immediate fund transfers 24/7, enhancing financial flexibility and customer convenience. Both systems leverage secure banking networks to ensure safe, reliable, and efficient money movement across participating banks.

Key Terms

Settlement Time

NEFT processes transactions in hourly batches with settlement times typically ranging from 30 minutes to a few hours, depending on the time of day and bank processing cycles. Instant payments, such as IMPS or UPI, enable real-time fund transfers with settlements occurring within seconds, enhancing liquidity and cash flow efficiency. Explore detailed comparisons to understand which payment method best suits your financial needs and transaction urgency.

Real-Time Processing

NEFT processes electronic funds transfers in hourly batches, resulting in delayed settlement times, whereas instant payments enable real-time fund transfers within seconds, enhancing liquidity and transaction speed. The Reserve Bank of India's introduction of the Immediate Payment Service (IMPS) and Unified Payments Interface (UPI) platforms has revolutionized instant payments, surpassing NEFT in convenience and accessibility. Discover how real-time processing in instant payments transforms financial transactions and improves user experience.

Transaction Limits

NEFT (National Electronic Funds Transfer) supports bulk transactions with no minimum amount but has a transaction limit typically capped at Rs2 lakhs per transfer, processing payments in half-hourly batches during banking hours. Instant payments, such as those via UPI or IMPS, enable immediate fund transfer 24/7 with higher transaction limits, often up to Rs5 lakhs, facilitating real-time settlement and enhanced convenience. Explore detailed comparisons to understand which payment method best suits your transaction size and timing requirements.

Source and External Links

What is NEFT: How NEFT Works, Full Form, NEFT Transfer ... - Paytm - NEFT (National Electronic Funds Transfer) is an electronic payment system in India, maintained by the Reserve Bank of India, that allows individuals and organizations to transfer funds between bank accounts in hourly batches throughout the day, with no transaction fees for online transfers.

National Electronic Funds Transfer - Wikipedia - NEFT enables bank customers in India to transfer funds between any two NEFT-enabled bank accounts electronically, with settlements processed in half-hourly batches around the clock and no minimum or maximum limit on transfer amounts.

Features and Benefits of NEFT National Electronic Fund Transfer - NEFT is a traditional, secure, and cost-effective online fund transfer method available 24/7 across India, with no charges for internet or mobile banking transactions and only nominal fees for branch-initiated transfers.