Carbon footprint accounting quantifies greenhouse gas emissions linked to business activities, focusing on environmental impact measurement and reduction strategies. Social accounting evaluates a company's social performance, including labor practices, community engagement, and ethical governance to assess overall societal contributions. Explore these accounting methods to understand how organizations balance ecological responsibilities with social accountability.

Why it is important

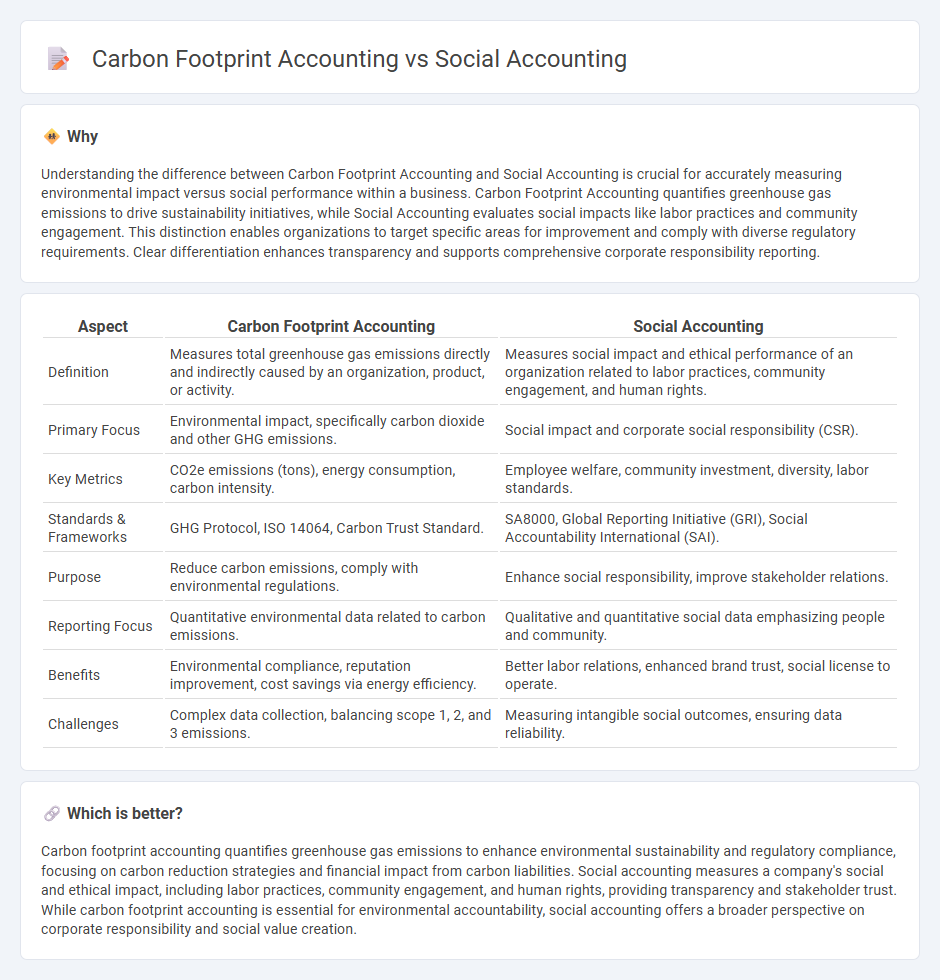

Understanding the difference between Carbon Footprint Accounting and Social Accounting is crucial for accurately measuring environmental impact versus social performance within a business. Carbon Footprint Accounting quantifies greenhouse gas emissions to drive sustainability initiatives, while Social Accounting evaluates social impacts like labor practices and community engagement. This distinction enables organizations to target specific areas for improvement and comply with diverse regulatory requirements. Clear differentiation enhances transparency and supports comprehensive corporate responsibility reporting.

Comparison Table

| Aspect | Carbon Footprint Accounting | Social Accounting |

|---|---|---|

| Definition | Measures total greenhouse gas emissions directly and indirectly caused by an organization, product, or activity. | Measures social impact and ethical performance of an organization related to labor practices, community engagement, and human rights. |

| Primary Focus | Environmental impact, specifically carbon dioxide and other GHG emissions. | Social impact and corporate social responsibility (CSR). |

| Key Metrics | CO2e emissions (tons), energy consumption, carbon intensity. | Employee welfare, community investment, diversity, labor standards. |

| Standards & Frameworks | GHG Protocol, ISO 14064, Carbon Trust Standard. | SA8000, Global Reporting Initiative (GRI), Social Accountability International (SAI). |

| Purpose | Reduce carbon emissions, comply with environmental regulations. | Enhance social responsibility, improve stakeholder relations. |

| Reporting Focus | Quantitative environmental data related to carbon emissions. | Qualitative and quantitative social data emphasizing people and community. |

| Benefits | Environmental compliance, reputation improvement, cost savings via energy efficiency. | Better labor relations, enhanced brand trust, social license to operate. |

| Challenges | Complex data collection, balancing scope 1, 2, and 3 emissions. | Measuring intangible social outcomes, ensuring data reliability. |

Which is better?

Carbon footprint accounting quantifies greenhouse gas emissions to enhance environmental sustainability and regulatory compliance, focusing on carbon reduction strategies and financial impact from carbon liabilities. Social accounting measures a company's social and ethical impact, including labor practices, community engagement, and human rights, providing transparency and stakeholder trust. While carbon footprint accounting is essential for environmental accountability, social accounting offers a broader perspective on corporate responsibility and social value creation.

Connection

Carbon footprint accounting quantifies greenhouse gas emissions associated with business activities, while social accounting measures a company's social impact on stakeholders and communities. Both accounting practices integrate environmental and social metrics to enhance sustainability reporting and corporate responsibility. This connection supports comprehensive ESG (Environmental, Social, and Governance) frameworks, driving transparent decision-making and stakeholder engagement.

Key Terms

Stakeholder Reporting

Social accounting emphasizes measuring a company's social impact on stakeholders, including employees, communities, and customers, capturing metrics like labor practices and community engagement. Carbon footprint accounting specifically quantifies greenhouse gas emissions across an organization's operations, providing detailed data crucial for environmental stakeholder reporting. Explore the distinctions between these frameworks to enhance transparent and comprehensive stakeholder communication.

Environmental Impact

Social accounting evaluates a company's overall environmental, social, and governance (ESG) performance by tracking sustainable practices and stakeholder impact, while carbon footprint accounting specifically measures greenhouse gas emissions associated with organizational activities. Carbon footprint accounting provides quantifiable data on CO2 equivalent emissions, essential for regulatory compliance and carbon reduction strategies. Explore more insights on how these accounting methods drive environmental responsibility and sustainable business practices.

Greenhouse Gas Emissions

Social accounting measures a company's impact on society, including labor practices and community engagement, while carbon footprint accounting quantifies greenhouse gas emissions from activities such as energy use and transportation. Carbon footprint accounting specifically tracks emissions of CO2, CH4, and N2O to help organizations reduce their climate impact through sustainability initiatives. Explore detailed comparisons and methodologies to understand how both approaches contribute to environmental and social responsibility.

Source and External Links

The Difference between Social Accounting and Social Auditing - Social accounting is a systematic process of measuring, reporting, and verifying the social and environmental impacts of an organization's operations, emphasizing transparency and accountability to stakeholders.

Social accounting - Wikipedia - Social accounting involves communicating the social and environmental effects of an organization's economic actions, often linked to corporate social responsibility (CSR), to various stakeholders and society at large.

Social Accounting: A Practical Guide - Community-Wealth.org - Social accounting typically follows a three-step process: planning/scoping, accounting, and reporting/auditing, adapted to organization size and capacity, with support frameworks such as the Social Audit Network in the UK.