Dynamic allocation tracing tracks costs by following resource consumption patterns in real-time, offering precise expense attribution across departments or activities. Resource-based costing assigns costs based on predefined metrics like labor hours or machine usage, providing a structured but less flexible approach to expense allocation. Explore the advantages of each method to optimize your accounting strategies and enhance financial accuracy.

Why it is important

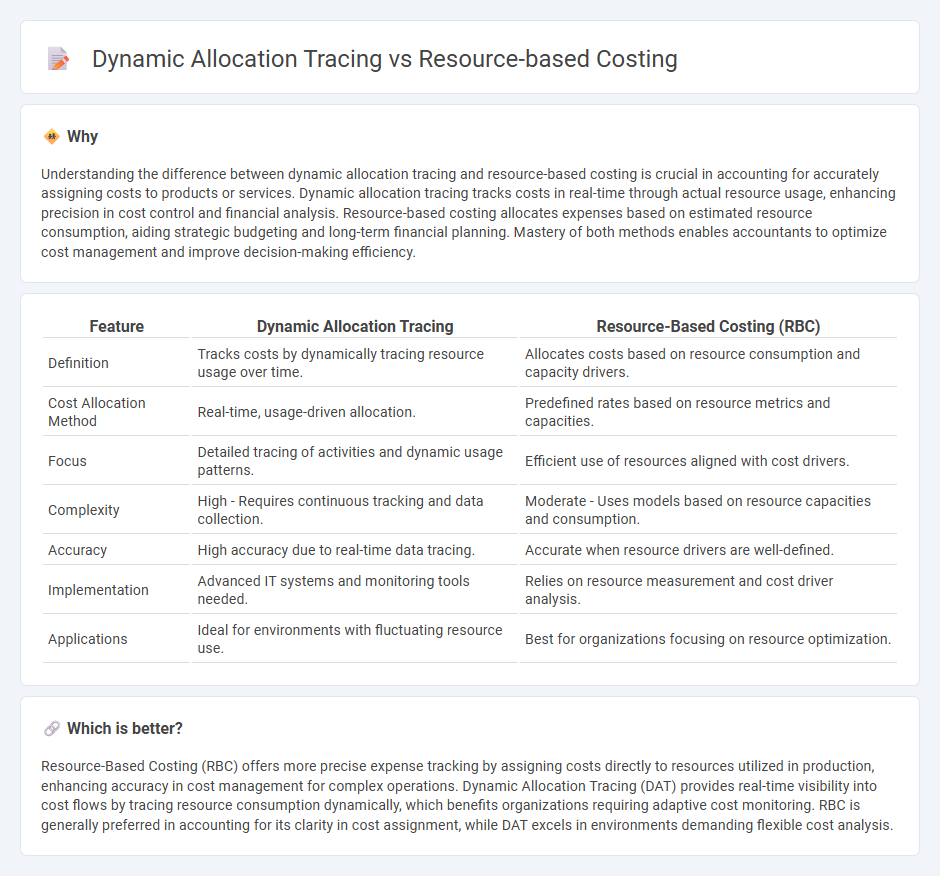

Understanding the difference between dynamic allocation tracing and resource-based costing is crucial in accounting for accurately assigning costs to products or services. Dynamic allocation tracing tracks costs in real-time through actual resource usage, enhancing precision in cost control and financial analysis. Resource-based costing allocates expenses based on estimated resource consumption, aiding strategic budgeting and long-term financial planning. Mastery of both methods enables accountants to optimize cost management and improve decision-making efficiency.

Comparison Table

| Feature | Dynamic Allocation Tracing | Resource-Based Costing (RBC) |

|---|---|---|

| Definition | Tracks costs by dynamically tracing resource usage over time. | Allocates costs based on resource consumption and capacity drivers. |

| Cost Allocation Method | Real-time, usage-driven allocation. | Predefined rates based on resource metrics and capacities. |

| Focus | Detailed tracing of activities and dynamic usage patterns. | Efficient use of resources aligned with cost drivers. |

| Complexity | High - Requires continuous tracking and data collection. | Moderate - Uses models based on resource capacities and consumption. |

| Accuracy | High accuracy due to real-time data tracing. | Accurate when resource drivers are well-defined. |

| Implementation | Advanced IT systems and monitoring tools needed. | Relies on resource measurement and cost driver analysis. |

| Applications | Ideal for environments with fluctuating resource use. | Best for organizations focusing on resource optimization. |

Which is better?

Resource-Based Costing (RBC) offers more precise expense tracking by assigning costs directly to resources utilized in production, enhancing accuracy in cost management for complex operations. Dynamic Allocation Tracing (DAT) provides real-time visibility into cost flows by tracing resource consumption dynamically, which benefits organizations requiring adaptive cost monitoring. RBC is generally preferred in accounting for its clarity in cost assignment, while DAT excels in environments demanding flexible cost analysis.

Connection

Dynamic allocation tracing enhances Resource-based costing by accurately tracking resource usage in real-time, enabling precise allocation of costs to specific activities or products. This method improves cost visibility, supporting more informed decision-making and efficient resource management within accounting systems. Integrating dynamic allocation tracing into Resource-based costing frameworks fosters greater accuracy in expense distribution and profitability analysis.

Key Terms

Cost Drivers

Resource-based costing identifies cost drivers by analyzing resource consumption patterns, linking costs to specific activities for precise expense management. Dynamic allocation tracing continuously monitors resource use in real-time, allowing for flexible and adaptive cost distribution based on changing operational demands. Explore the nuances of these methods to optimize your cost driver analysis effectively.

Resource Pools

Resource-based costing allocates expenses based on resource consumption within defined resource pools, enhancing accuracy in cost distribution for complex operations. Dynamic allocation tracing adapts cost assignment in real-time by tracing resource usage patterns, allowing for more granular and flexible financial analysis. Explore the detailed differences and practical applications of these methods for optimized resource management.

Cost Allocation Methods

Resource-based costing allocates costs by identifying resources consumed by each activity and assigning expenses proportionally, enhancing accuracy in overhead distribution. Dynamic allocation tracing tracks real-time resource usage, offering a flexible, responsive approach to cost assignment that adapts to operational changes. Explore detailed comparisons and practical applications of these cost allocation methods to optimize your financial management strategies.

Source and External Links

Understanding costs: Part 2 -- resource-based costing - FM - Resource-based costing is a detailed approach where costs are first linked to specific resources, then allocated to activities consuming those resources, and finally assigned to cost objects, providing valuable insights for operational and strategic management despite potential complexity in its development and maintenance.

Resource Cost Allocation Method Explained - Teamhub.com - Resource cost allocation involves assigning costs to activities, departments, or products based on their resource usage, guided by principles such as causality, objectivity, and consistency to ensure fairness and accuracy in cost management.

Resource Costing - Documentation Center | CompuTec Learn - Resource costing calculates the cost of resource activities during production by assigning hourly rates for labor and machines, using configured financial accounts for cost tracking and posting, supporting detailed cost management in manufacturing processes.