Carbon footprint accounting measures the total greenhouse gas emissions caused directly and indirectly by an organization, product, or activity, focusing on carbon dioxide equivalents to assess environmental impact. Resource accounting tracks the consumption and depletion of natural resources, including water, minerals, and energy, providing a broader perspective on sustainability and ecosystem strain. Explore deeper insights into how these accounting methods drive sustainable business practices and environmental responsibility.

Why it is important

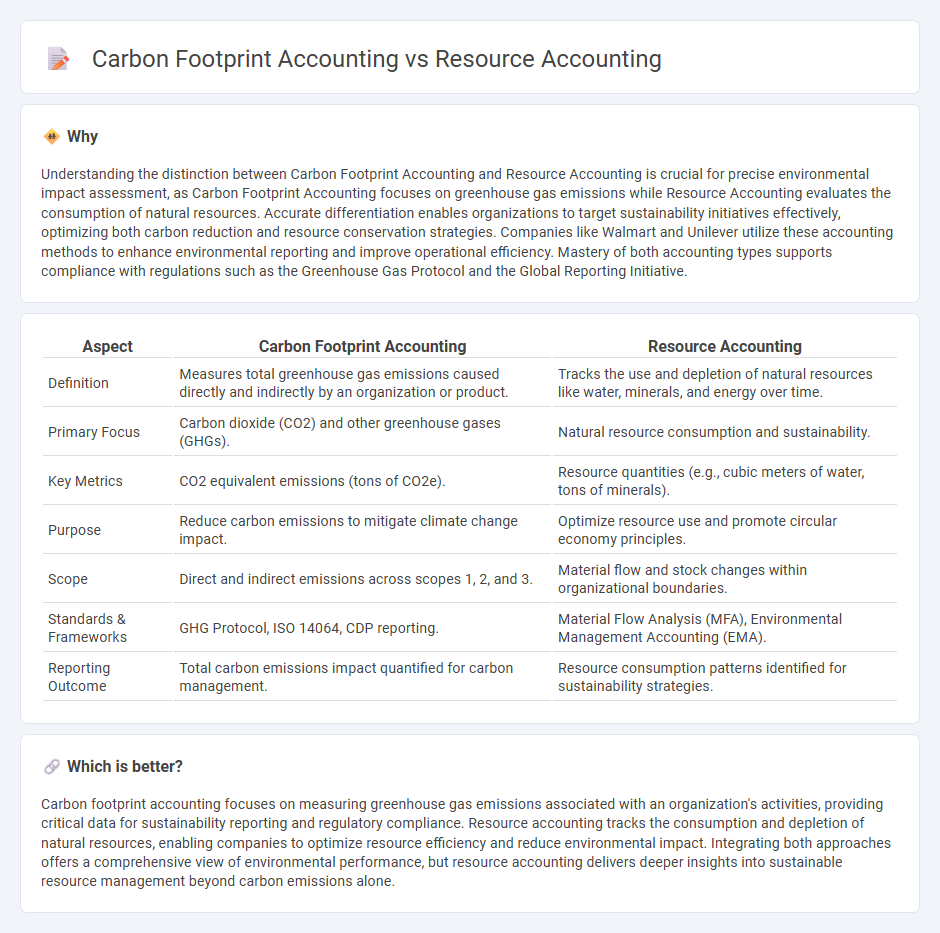

Understanding the distinction between Carbon Footprint Accounting and Resource Accounting is crucial for precise environmental impact assessment, as Carbon Footprint Accounting focuses on greenhouse gas emissions while Resource Accounting evaluates the consumption of natural resources. Accurate differentiation enables organizations to target sustainability initiatives effectively, optimizing both carbon reduction and resource conservation strategies. Companies like Walmart and Unilever utilize these accounting methods to enhance environmental reporting and improve operational efficiency. Mastery of both accounting types supports compliance with regulations such as the Greenhouse Gas Protocol and the Global Reporting Initiative.

Comparison Table

| Aspect | Carbon Footprint Accounting | Resource Accounting |

|---|---|---|

| Definition | Measures total greenhouse gas emissions caused directly and indirectly by an organization or product. | Tracks the use and depletion of natural resources like water, minerals, and energy over time. |

| Primary Focus | Carbon dioxide (CO2) and other greenhouse gases (GHGs). | Natural resource consumption and sustainability. |

| Key Metrics | CO2 equivalent emissions (tons of CO2e). | Resource quantities (e.g., cubic meters of water, tons of minerals). |

| Purpose | Reduce carbon emissions to mitigate climate change impact. | Optimize resource use and promote circular economy principles. |

| Scope | Direct and indirect emissions across scopes 1, 2, and 3. | Material flow and stock changes within organizational boundaries. |

| Standards & Frameworks | GHG Protocol, ISO 14064, CDP reporting. | Material Flow Analysis (MFA), Environmental Management Accounting (EMA). |

| Reporting Outcome | Total carbon emissions impact quantified for carbon management. | Resource consumption patterns identified for sustainability strategies. |

Which is better?

Carbon footprint accounting focuses on measuring greenhouse gas emissions associated with an organization's activities, providing critical data for sustainability reporting and regulatory compliance. Resource accounting tracks the consumption and depletion of natural resources, enabling companies to optimize resource efficiency and reduce environmental impact. Integrating both approaches offers a comprehensive view of environmental performance, but resource accounting delivers deeper insights into sustainable resource management beyond carbon emissions alone.

Connection

Carbon footprint accounting quantifies greenhouse gas emissions associated with business activities, while resource accounting tracks the consumption of natural resources such as water, minerals, and energy. Both accounting methods share a focus on sustainability metrics, enabling companies to assess environmental impact comprehensively and identify areas for reducing waste and emissions. Integrating these practices supports transparent environmental reporting and drives efficient resource management aligned with corporate social responsibility goals.

Key Terms

Asset Valuation

Resource accounting quantifies the consumption and depletion of natural assets, emphasizing the valuation of resources as tangible economic assets subject to depreciation and renewal costs. Carbon footprint accounting measures greenhouse gas emissions linked to assets, integrating environmental costs into asset valuation by monetizing carbon impacts and regulatory risks. Explore how these accounting approaches reshape financial assessments and investment decisions for sustainable asset management.

Emission Factors

Resource accounting and carbon footprint accounting differ in scope and application, with resource accounting emphasizing comprehensive tracking of material and energy inputs and outputs, while carbon footprint accounting specifically measures greenhouse gas emissions using emission factors derived from standardized databases like IPCC or EPA. Emission factors in carbon footprint accounting quantify the average emissions released per unit of activity or product, facilitating more precise carbon impact assessments and enabling targeted emissions reduction strategies. Explore further to understand how emission factors influence sustainability metrics and decision-making frameworks.

Double-Entry Bookkeeping

Resource accounting tracks the consumption and replenishment of natural resources using double-entry bookkeeping to ensure balanced environmental and economic records. Carbon footprint accounting quantifies greenhouse gas emissions associated with activities, integrating these metrics into financial statements through dual ledger entries for accuracy and transparency. Discover how double-entry bookkeeping enhances precision in sustainability reporting by exploring these accounting methodologies further.

Source and External Links

Resource Accounting Key to Savings - This resource accounting system is designed to manage and reduce resource costs by tracking usage and costs of resources like electricity, water, and fossil fuels.

Resource Accounting and Budgeting (RAB) - RAB is a system used by governments for planning, controlling, and reporting public spending, focusing on efficient resource allocation.

Resource Accounting for z/OS - This system helps manage data processing costs by distributing them equitably among customers, supporting both cost centers and profit centers within organizations.