Outcome-based budgeting focuses on allocating resources to achieve specific organizational results, emphasizing performance measurement and accountability. Activity-based budgeting allocates funds according to detailed activities and processes, aiming to enhance cost efficiency by analyzing each task's expenses. Explore the detailed differences to understand which budgeting approach suits your financial management needs best.

Why it is important

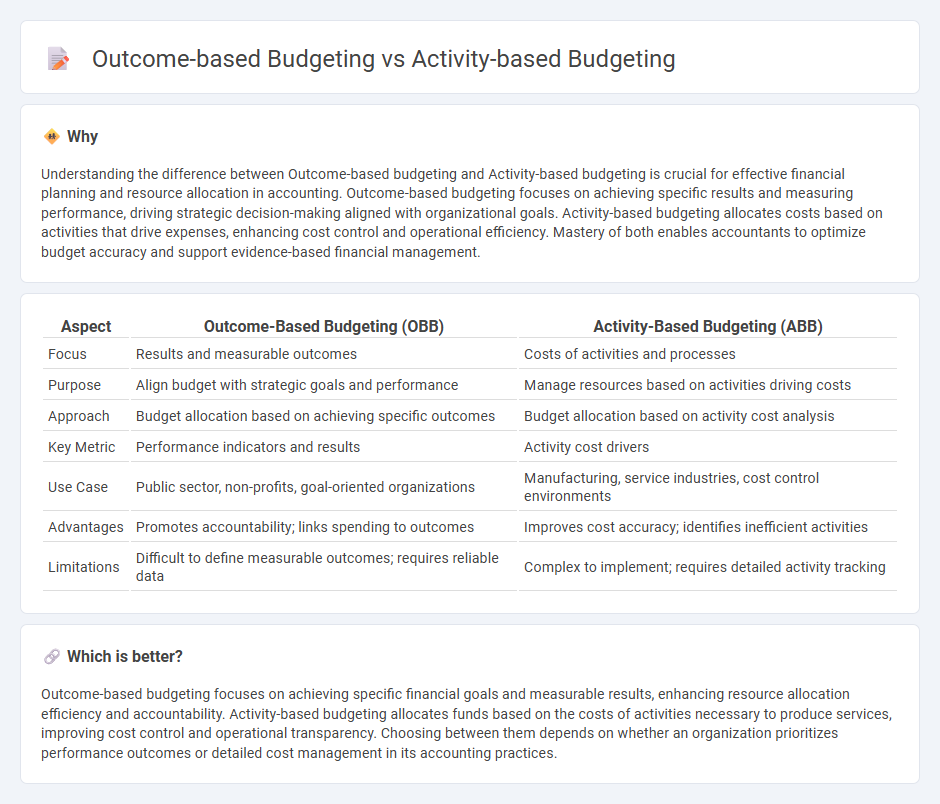

Understanding the difference between Outcome-based budgeting and Activity-based budgeting is crucial for effective financial planning and resource allocation in accounting. Outcome-based budgeting focuses on achieving specific results and measuring performance, driving strategic decision-making aligned with organizational goals. Activity-based budgeting allocates costs based on activities that drive expenses, enhancing cost control and operational efficiency. Mastery of both enables accountants to optimize budget accuracy and support evidence-based financial management.

Comparison Table

| Aspect | Outcome-Based Budgeting (OBB) | Activity-Based Budgeting (ABB) |

|---|---|---|

| Focus | Results and measurable outcomes | Costs of activities and processes |

| Purpose | Align budget with strategic goals and performance | Manage resources based on activities driving costs |

| Approach | Budget allocation based on achieving specific outcomes | Budget allocation based on activity cost analysis |

| Key Metric | Performance indicators and results | Activity cost drivers |

| Use Case | Public sector, non-profits, goal-oriented organizations | Manufacturing, service industries, cost control environments |

| Advantages | Promotes accountability; links spending to outcomes | Improves cost accuracy; identifies inefficient activities |

| Limitations | Difficult to define measurable outcomes; requires reliable data | Complex to implement; requires detailed activity tracking |

Which is better?

Outcome-based budgeting focuses on achieving specific financial goals and measurable results, enhancing resource allocation efficiency and accountability. Activity-based budgeting allocates funds based on the costs of activities necessary to produce services, improving cost control and operational transparency. Choosing between them depends on whether an organization prioritizes performance outcomes or detailed cost management in its accounting practices.

Connection

Outcome-based budgeting and Activity-based budgeting are connected through their focus on aligning financial resources with organizational goals and activities. Outcome-based budgeting allocates funds based on the desired results or outcomes, while Activity-based budgeting assigns costs to specific activities to ensure efficient resource utilization. Together, they enhance financial planning by linking expenditures directly to performance metrics and operational processes.

Key Terms

Cost Drivers

Activity-based budgeting allocates funds based on the specific activities and cost drivers that contribute to organizational expenses, enabling precise tracking and efficient resource allocation. Outcome-based budgeting, on the other hand, prioritizes funding according to the results or outcomes desired, linking expenditures directly to performance targets and strategic goals. Discover how these budgeting methods optimize financial planning by focusing on cost drivers and results.

Performance Metrics

Activity-based budgeting allocates funds based on specific operational activities, ensuring resources are directed towards processes that drive costs and efficiency. Outcome-based budgeting prioritizes financial planning around measurable results and performance metrics, linking expenditures directly to desired programmatic achievements. Explore the advantages and implementation strategies of each budgeting approach to enhance fiscal performance management.

Resource Allocation

Activity-based budgeting allocates resources based on specific organizational activities, ensuring funds are directly tied to operational tasks and cost drivers, promoting efficiency and accountability. Outcome-based budgeting directs resources towards achieving predefined goals or results, emphasizing performance measurement and strategic impact over process details. Explore deeper insights to understand which budgeting approach best aligns with your organization's resource optimization and goal-setting needs.

Source and External Links

Activity-Based Budgeting (ABB) Explained - Activity-based budgeting involves closely examining every cost associated with an activity to create a more granular budget, focusing on resource allocation and efficiency.

What is Activity-Based Budgeting (ABB)? - Activity-based budgeting identifies and allocates resources based on activities required to achieve company goals, ensuring financial resources are optimized for strategic objectives.

Activity-Based Budgeting: Definition, Benefits and Example - Activity-based budgeting is a comprehensive budgeting system that records and analyzes every activity to find areas for improving efficiencies and reducing costs.