Outcome-based budgeting allocates resources by focusing on measurable results and specific performance outcomes, ensuring funds directly support organizational goals. Priority-based budgeting ranks programs and services by importance to align spending with strategic priorities, enabling more effective resource distribution. Explore the key differences and benefits of each budgeting approach to optimize financial planning.

Why it is important

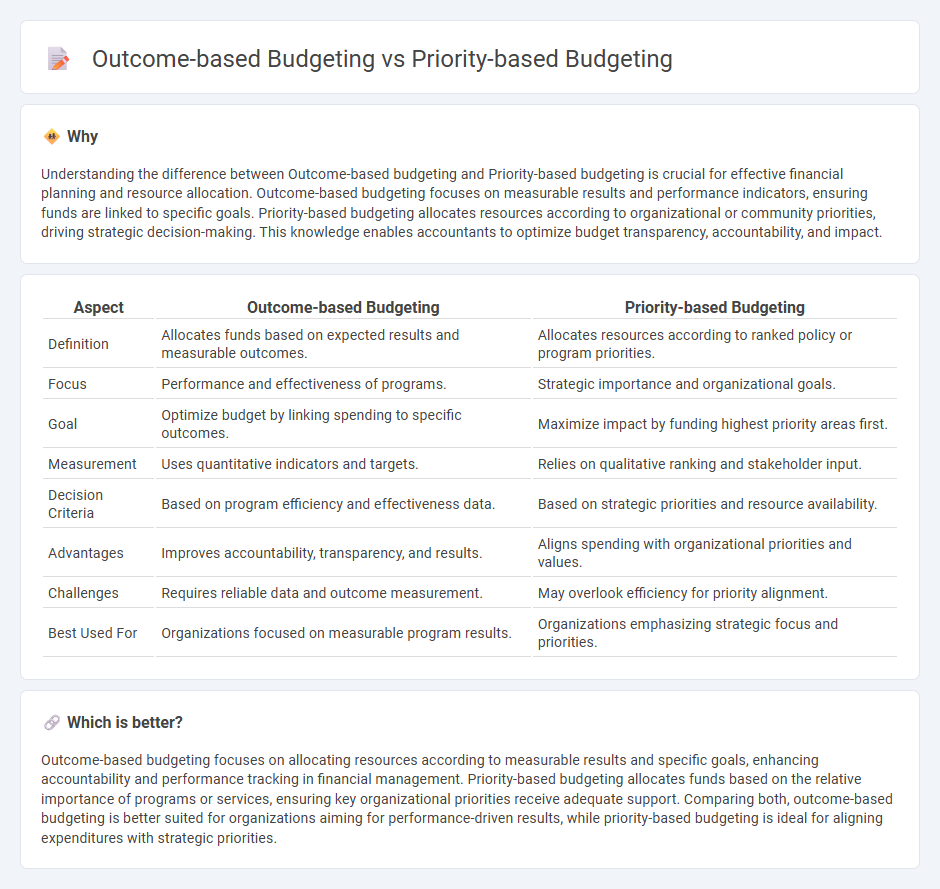

Understanding the difference between Outcome-based budgeting and Priority-based budgeting is crucial for effective financial planning and resource allocation. Outcome-based budgeting focuses on measurable results and performance indicators, ensuring funds are linked to specific goals. Priority-based budgeting allocates resources according to organizational or community priorities, driving strategic decision-making. This knowledge enables accountants to optimize budget transparency, accountability, and impact.

Comparison Table

| Aspect | Outcome-based Budgeting | Priority-based Budgeting |

|---|---|---|

| Definition | Allocates funds based on expected results and measurable outcomes. | Allocates resources according to ranked policy or program priorities. |

| Focus | Performance and effectiveness of programs. | Strategic importance and organizational goals. |

| Goal | Optimize budget by linking spending to specific outcomes. | Maximize impact by funding highest priority areas first. |

| Measurement | Uses quantitative indicators and targets. | Relies on qualitative ranking and stakeholder input. |

| Decision Criteria | Based on program efficiency and effectiveness data. | Based on strategic priorities and resource availability. |

| Advantages | Improves accountability, transparency, and results. | Aligns spending with organizational priorities and values. |

| Challenges | Requires reliable data and outcome measurement. | May overlook efficiency for priority alignment. |

| Best Used For | Organizations focused on measurable program results. | Organizations emphasizing strategic focus and priorities. |

Which is better?

Outcome-based budgeting focuses on allocating resources according to measurable results and specific goals, enhancing accountability and performance tracking in financial management. Priority-based budgeting allocates funds based on the relative importance of programs or services, ensuring key organizational priorities receive adequate support. Comparing both, outcome-based budgeting is better suited for organizations aiming for performance-driven results, while priority-based budgeting is ideal for aligning expenditures with strategic priorities.

Connection

Outcome-based budgeting and priority-based budgeting are connected through their focus on aligning financial resources with organizational goals to enhance efficiency and effectiveness. Outcome-based budgeting allocates funds based on measurable results and performance indicators, while priority-based budgeting ranks expenditures according to strategic importance and desired outcomes. Both approaches emphasize data-driven decision-making to optimize resource allocation and improve fiscal responsibility in accounting and public finance.

Key Terms

Resource Allocation

Priority-based budgeting allocates resources according to an organization's key objectives, ensuring funds are directed to high-priority areas that align with strategic goals. Outcome-based budgeting ties financial resources directly to measurable results and performance indicators, promoting accountability and efficiency in achieving desired outcomes. Explore these budgeting approaches further to understand which method best optimizes your resource allocation strategy.

Performance Metrics

Priority-based budgeting allocates funds according to strategic importance and organizational priorities, emphasizing resource distribution to high-impact areas. Outcome-based budgeting measures success through performance metrics and results, focusing on achieving specific goals and assessing program effectiveness. Explore how these budgeting approaches influence financial planning and drive performance outcomes.

Budget Justification

Priority-based budgeting allocates resources according to ranked importance of programs, ensuring funds align with strategic goals and stakeholder priorities. Outcome-based budgeting emphasizes measurable results and performance indicators to justify expenditures, linking budget requests directly to program effectiveness. Explore how each approach enhances budget justification and drives fiscal accountability.

Source and External Links

The Advantages and Disadvantages of Priority Based Budgeting - Discusses the benefits and drawbacks of priority-based budgeting, including its focus on service areas and outcomes over traditional line items.

Anatomy of a Priority-Driven Budget Process - Outlines the eight major steps involved in implementing a priority-driven budget process.

Priority Based Budgeting - Describes how priority-based budgeting allocates funds based on community priorities and available resources, rather than departments or historical expenditures.